Low Inventory Maintaining a Ground Underneath Property Costs

by thebestworldevents.com 4 February 2024 · Property Investment

[ad_1]

The declines in property costs have slowed down for now, with the most recent information from

CoreLogic displaying the smallest month-to-month fall since Might 2022.

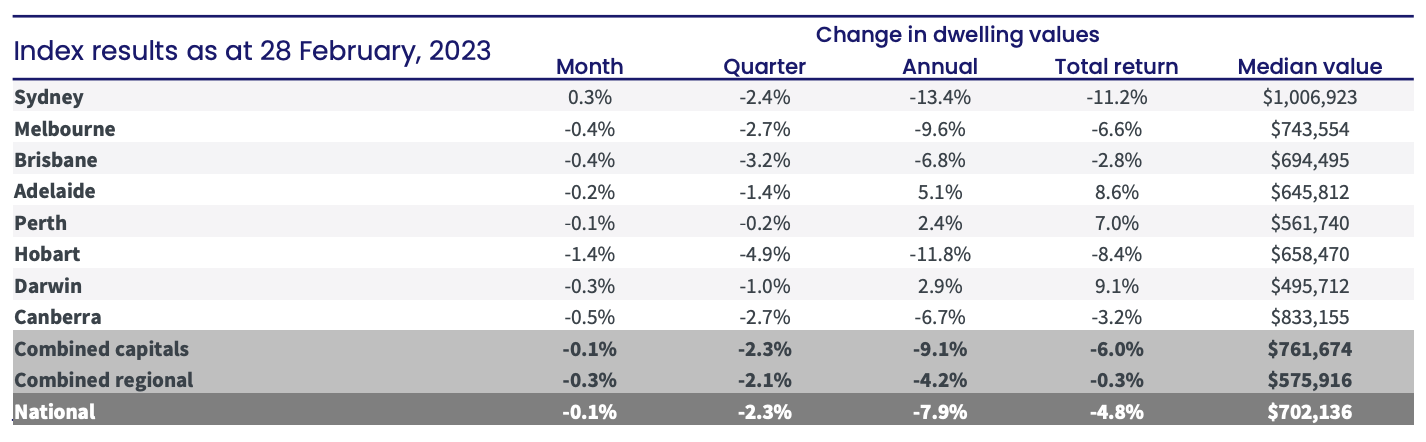

Nationwide property costs declined simply 0.14% over the month of February, with Sydney

main the turnaround on the again of a 0.3% enhance within the median value. All different capital cities recorded falling values in February, with Melbourne and Brisbane each declining 0.4%, Canberra down 0.5%, Darwin 0.4%, Adelaide 0.2% and Perth 0.1% whereas Hobart had the largest drop, tumbling 1.4%.

CoreLogic’s analysis director, Tim Lawless, stated the stabilisation in housing values over the month coincides with persistently low marketed provide ranges and an increase in public sale clearance charges.

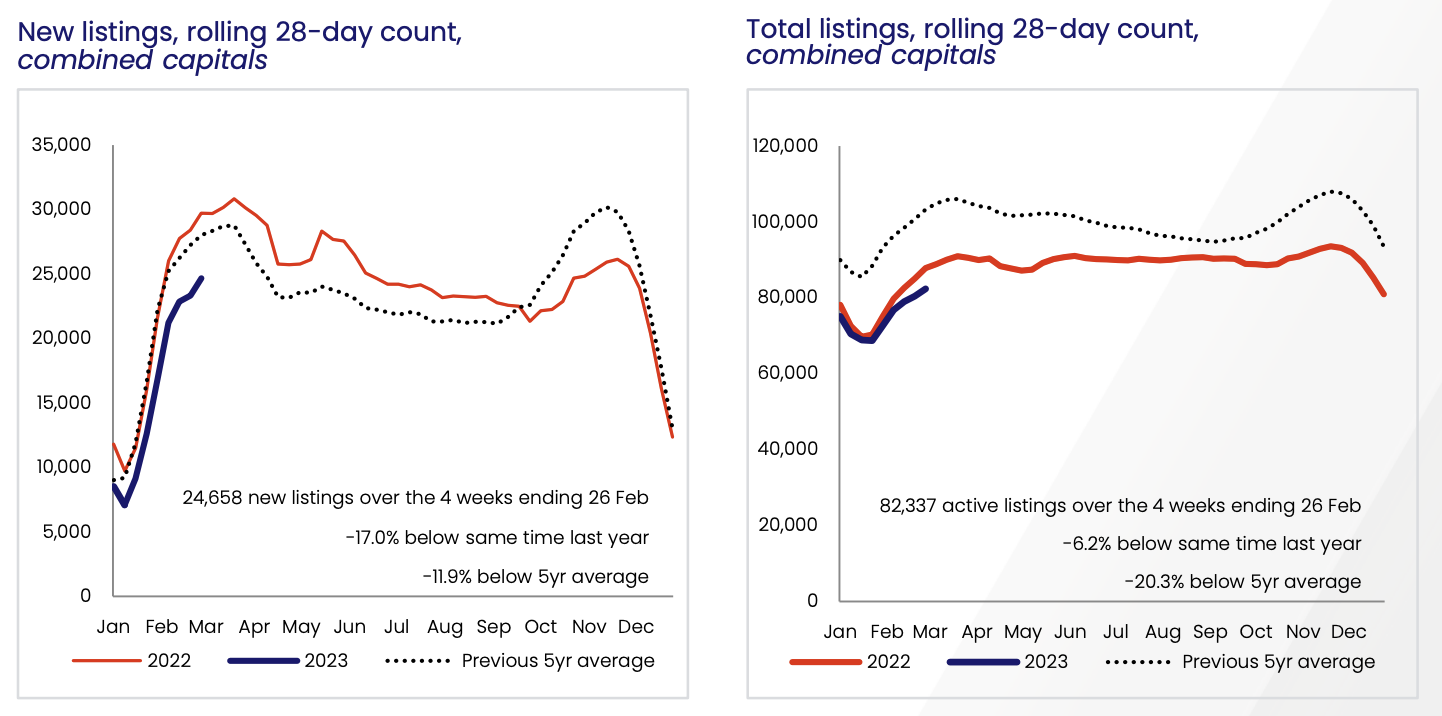

“The previous 4 weeks have seen the stream of latest capital metropolis listings monitoring 17.0% decrease than a 12 months in the past and 11.9% under the earlier five-year common,” Mr Lawless stated. “This pattern in direction of a under common stream of latest listings has been evident since September final 12 months, coinciding with a lack of momentum within the fee of worth decline.”

Supply: CoreLogic

Public sale clearance charges additionally bounced again final month, with the capital cities reaching the excessive 60% vary by means of the second half of the month, whereas Sydney clearance charges rose to above 70% for the primary time since February 2022.

The higher finish of the market within the capital cities drove this month’s stabilising pattern, rising by 0.1% in February. Whereas nonetheless falling, declines throughout the decrease finish of the market additionally stabilised, down 0.1%.

As soon as once more it was Sydney’s premium properties main the best way with a 0.7% rise in values over the month, in contrast with a 0.2% fall in values throughout the decrease quartile of the Sydney market.

In the meantime, regional costs had been down 0.3% in February in contrast with a 0.1% fall throughout the mixed capital cities. Since peaking in June final 12 months, the mixed regionals index is down 7.7%, in contrast with a 9.7% drop within the mixed capital cities index, which peaked barely earlier in April 2022.

Regardless of the optimistic end result, Mr Lawless warned that the uptick in costs may not final.

“Contemplating the RBA’s transfer to a extra hawkish stance on the February board assembly, together with an expectation for a weaker financial efficiency and a loosening in labour markets, there’s a good probability this reprieve within the housing downturn could possibly be short-lived,” Mr Lawless stated.

“We even have the fixed-rate cliff forward of us; arguably the total impression of the aggressive fee climbing cycle is but to play out.”

Listings stay low

One of many predominant components contributing to the soar within the nationwide index has been the tight degree of inventory in the marketplace.

Throughout February, there was a notable rise within the variety of new listings, rising by roughly 11,250 greater than the earlier month. Nevertheless, that is nonetheless 12.6% under the earlier five-year common for this time of 12 months.

“Up to now, it appears potential distributors are ready to attend this downturn out,” Mr Lawless stated.

“The stream of latest listings is nicely under common for this time of the 12 months throughout every of the foremost capitals. The stream of latest listings can be a key pattern to observe over the approaching months.”

“Any indicators of listings exercise transferring to above common ranges may weigh on housing costs.”

Supply: CoreLogic

Unit rents are surging

Based on CoreLogic, the very best rental development is now occurring within the unit sector throughout the three largest capitals, led by a 16.7% soar in Sydney unit rents over the previous 12 months.

“Though unit rents within the largest cities confirmed a interval of weak spot by means of the early part of the pandemic, weekly rental values for items at the moment are 19.0% greater than on the onset of COVID in Sydney, 10.4% greater throughout Melbourne and 23.6% up in Brisbane,” Mr Lawless stated.

“A number of components are more likely to be contributing to the surge in unit rents.

“Rental affordability pressures could also be forcing a transition of demand in direction of greater density rental choices.

“Moreover, the robust rebound in overseas pupil and worldwide migrant arrivals could be including to rental demand, significantly in internal metropolis precincts in addition to areas inside shut proximity to universities and transport hubs.”

Draw back threat stays

Mr Lawless stated regardless of the current pattern in direction of stabilisation, housing dangers stay skewed to the draw back.

The February housing market efficiency instructed some renewed power in market situations, whereas the stream of latest listings has been at below-average ranges since September final 12 months, which has helped to help a discount within the tempo of worth falls.

However, it’s most likely too early to name a trough within the cycle contemplating there are a number of components which may set off a ‘re-acceleration’ of housing worth declines over the course of the 12 months.

On the again of the most recent enhance within the money fee, Mr Lawless stated there are nonetheless extra fee hikes anticipated over the course of the 12 months, and an additional decline in borrowing capability is on the playing cards, which may reaccelerate housing market declines.

Low marketed inventory ranges are more likely to persist as householders resist promoting in a declining market. Nevertheless, there could also be a small portion of potential distributors who change into extra motivated or are compelled to promote amid rising challenges to serviceability.

These challenges embrace an ongoing enhance in rates of interest, extra debtors being uncovered to greater charges as the vast majority of fastened phrases finish, rising unemployment and a better value of residing.

Mr Lawless stated long run, the market is poised for restoration and regardless of the headwinds accumulating for the housing market in 2023, there isn’t any denying the elemental under-supply of housing inventory.

[ad_2]