How A lot is That $70,000 Truck Costing You?

by thebestworldevents.com 2 February 2024 · Wealth Management

[ad_1]

A reader asks:

I work within the building trade and I’m at all times making an attempt to unfold somewhat monetary literacy to my coworkers. Each time I see a younger man on the brink of drop $70k on a brand new pickup I attempt to present them what that cash may turn out to be in the event that they invested in index funds as an alternative. I prefer to name it “sequence of spending threat”. In fact this hardly ever works so I believed having the consultants remark may assist. Possibly you could possibly provide you with a chart or graphic that would clarify how delaying spending may have a huge impact on future wealth.

I used to be born for this query.

I’ve written numerous posts through the years about extreme spending on vans and SUVs:

I’m not a fan of spend-shaming…UNLESS you’re spending method an excessive amount of on one thing AND not saving any cash.

You must take pleasure in your self if you’re younger however you additionally have to develop good financial savings habits as a result of the compounding results are so sturdy.

So how a lot may that $70k truck be costing these younger building employees?

I poked round somewhat and located new automotive mortgage charges at round 6% or greater proper now.

Financing a $70,000 truck at 6% over 5 years can be a month-to-month fee of $1,350 (assuming nothing down).

That’s a ridiculously excessive month-to-month fee for most individuals however particularly younger folks due to the chance prices.

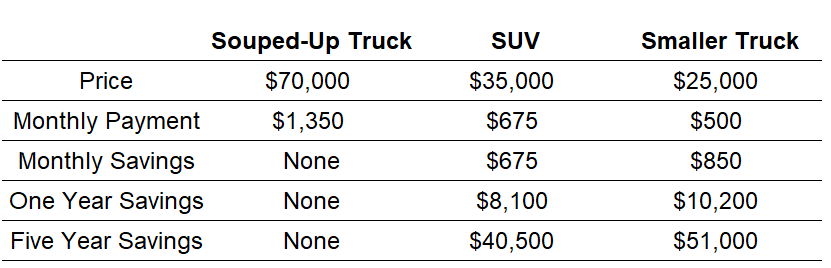

Let’s say as an alternative of that Ford F-150 or Dodge Ram you as an alternative obtained your self a fairly priced SUV, possibly one thing like a Ford Explorer or Chevy Trailblazer.

That in all probability cuts your value in half to $35,000 or so relying on the facilities.1

You’d save $675 a month or greater than $8,000 in a yr. Over the course of a five-year mortgage, that’s a complete financial savings of greater than $40,000.

Are you able to think about the expansion of $40,000 over the course of two to 3 many years for a youngster should you invested that cash as an alternative of spending it on a souped-up truck?!

We’ll get to these numbers however let’s say you do want a truck since you work in building and might’t make one other car work.

The Ford Maverick has an MSRP of round $25,000. Now we’re a month-to-month fee of extra like $500. I’m not even telling you to get a used automotive. I’m simply saying I don’t get the top-of-the-line, suped-up truck in the marketplace.

That’s a financial savings of $850 a month. That may offer you greater than ten grand in annual financial savings, sufficient to replenish practically half of your annual 401k max restrict. Over 5 years we’re $51,000 in financial savings.

And it’s nonetheless a truck!

Right here’s the breakdown:

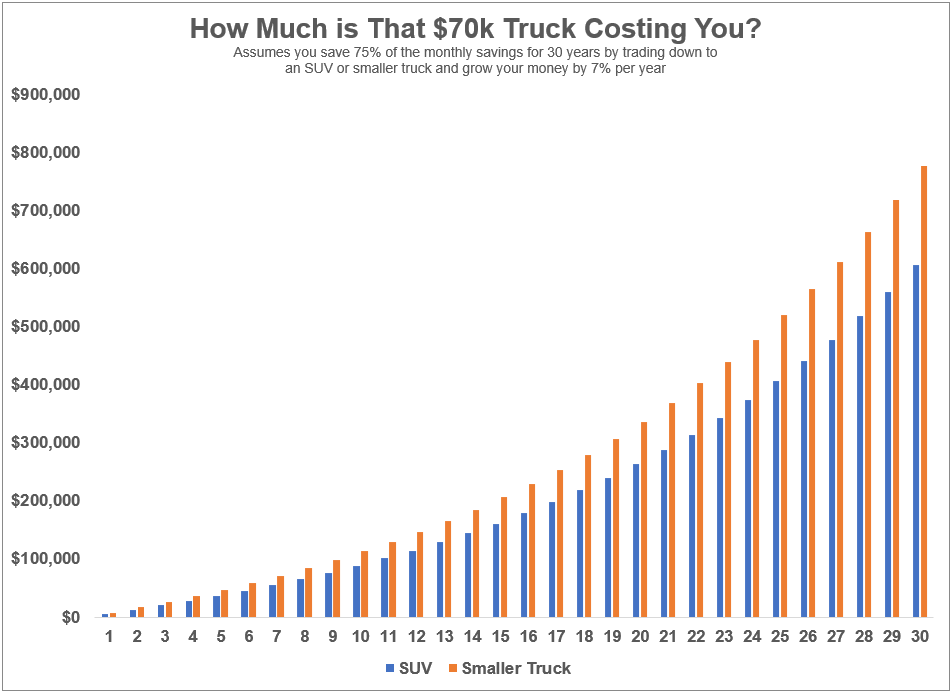

Now let’s do the private finance factor and have a look at how a lot these financial savings might be value over the lengthy haul.

Let’s say you say simply 75% of the month-to-month financial savings so you may blow the remainder of the cash on anything you’d like.

Right here’s what it appears like should you financial institution these financial savings within the inventory market yearly for 30 years and earn 7% in your investments:

You’re someplace within the $600k to $800k vary in complete from simply driving a lower-priced car over time. That’s fairly eye-opening.

However let’s be sincere, this instance in all probability isn’t all that lifelike. If you happen to’re an enormous truck particular person you’re going to need a huge truck ultimately, no matter what the spreadsheets say.

OK tremendous, however what should you simply wait till you’re somewhat older to purchase a truck that may pull a 747?

Let’s say you’re a 25-year-old building employee who drives a smaller truck or an SUV for one mortgage cycle. All you must do is wait till you’re 30 to purchase a tank on wheels.

Right here’s a have a look at what simply 5 years’ value of financial savings would develop into over 30 years in complete:

This assumes you financial institution 75% of the month-to-month financial savings from an SUV or smaller truck into the inventory market after which let it compound from there. Now we’re speaking extra like 1 / 4 of 1,000,000 {dollars} after 30 years from simply 5 years of driving a lower-priced car.

Possibly it’s not lifelike to imagine you may hold saving that distinction yr after yr for thus lengthy. Finally you’re in all probability going to wish to splurge on that vast truck.

I’m not a kind of private finance consultants who likes to do that with each buy. You must be capable of take pleasure in your cash.

However it may be exhausting for younger folks to avoid wasting. And it’s not appetizers or drinks with buddies that may shoot a gap in your price range; it’s the massive fastened bills. For most individuals your largest fastened prices are housing and transportation.

If you happen to lock in excessive housing and transportation prices it doesn’t matter what number of lattes you skip from Starbucks.

I’ve no downside with spending cash on vans or automobiles or boats or jet skis or no matter so long as you’re saving cash. Prioritization is the hallmark of any good monetary plan.

However locking in a four-figure month-to-month fee if you’re younger is a poor alternative particularly should you’re not saving a lot for retirement. You must spend a few of your hard-earned cash however that doesn’t imply it is best to really feel entitled to a $70k car so early in your profession.

In fact, it’s not sufficient to easily purchase a lower-cost car. You even have to avoid wasting the distinction.

Automate these financial savings identical to you’d for the month-to-month automotive fee and also you’ll be set.

A six-figure Roth IRA account will do extra heavy lifting for you than a Ford F-150.

We coated this query on the most recent version of Ask the Compound:

My very own monetary advisor Invoice Candy joined the present once more this week to assist me sort out questions on faculty financial savings, the tax implications of investing in bonds, max contribution limits for retirement accounts and what number of 529 plans you want in your youngsters.

1And let’s be sincere — should you’re a youngster you don’t want all of the bells and whistles relating to facilities. When you get them they’re going to turn out to be a necessity, not a need.