A Nearer Take a look at Annuity Charges and Taxation

by thebestworldevents.com 3 February 2024 · Retirement

In response to Darrow’s current put up on inheriting an annuity, I acquired the next remark, which I edited for readability:

I’ve a variable annuity through Constancy. It’s the results of a 1035 conversion of a complete life insurance coverage product I want I hadn’t purchased in my late 30’s…..I pay .1% (for a) Constancy VIP Index plus .25% annual annuity cost for a complete of .35%…..For comparability FXAIX (Constancy’s S&P 500 index) fees .015% or .335% lower than the annuity model. Thus it’s $335 costlier per 12 months per $100,000 invested.

The variable annuity is best than the entire life product! I’m glad I used to be in a position to flip lemons into lemonade.

Would I purchase it once more by itself deserves? Sure!….I’m certain I’m lacking one thing as a result of everybody else is so unfavorable on them.

This remark highlights a superb technique for many who have been bought annuity and insurance coverage merchandise they remorse shopping for, the 1035 alternate. On a much less optimistic observe, the concept of shopping for an annuity by itself deserves highlights the misunderstanding of annuity charges and taxation that I believe are the rationale so many individuals find yourself with these merchandise that they later remorse. Let’s discover….

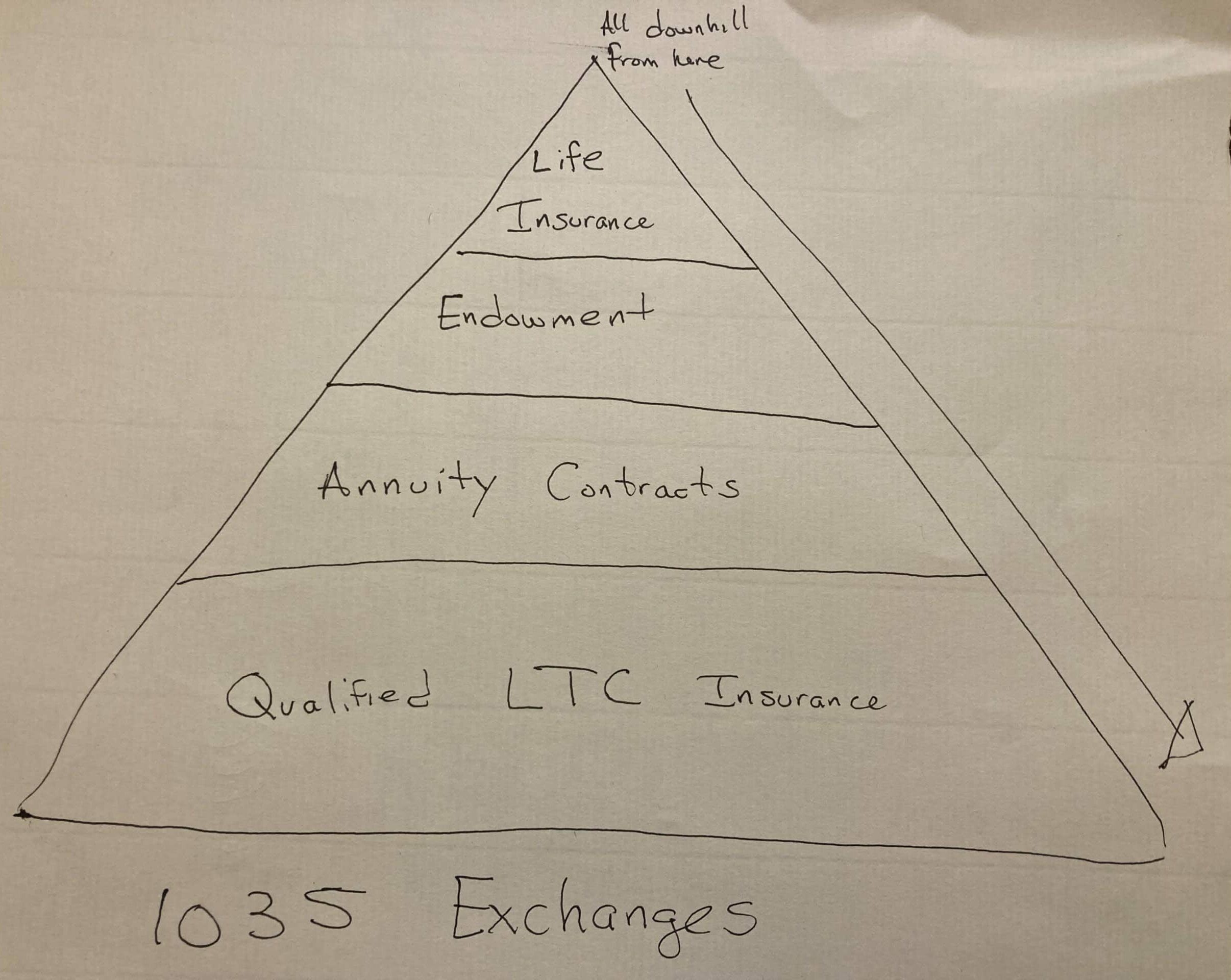

1035 Exchanges

Let’s begin with the a part of this remark that I really like, the 1035 alternate. Part 1035 is a bit of the IRS code that permits a tax-free alternate of 1 insurance coverage contract for an additional.

Part 1035 applies to life insurance coverage, endowments, and certified long-term care insurance coverage (LTC) insurance policies, in addition to annuities. I discovered the mnemonic system under that helped me when getting ready for my CFP examination:

Any of those insurance policies could be exchanged for a like type of coverage. Life insurance coverage insurance policies, on the prime of the pyramid, could be exchanged into one other life insurance coverage coverage or for any of the opposite coverage sorts under it on the pyramid. On the different excessive, LTC insurance policies, on the base of the pyramid, cannot be exchanged for something aside from one other LTC coverage.

Annuities, being close to the underside of the pyramid, are a preferred place to alternate undesirable, however generally bought, life insurance coverage merchandise or annuities. As such, there are merchandise generally termed “rescue annuities” as a result of they’re designed for the aim of rescuing shoppers from suboptimal merchandise they have been bought.

Vanguard used to supply a product for this which I exchanged my mother and father’ annuities into years in the past. They now not provide these merchandise. To my information, the Constancy annuity product referenced within the remark is the most suitable choice presently accessible.

When to Think about a 1035 Alternate

1035 exchanges work greatest with an insurance coverage contract that you just have been bought years or many years in the past outdoors of a professional account. On this situation, you’re sometimes out of any give up interval that will forestall you from exiting the contract.

Nonetheless, you could have amassed substantial taxable features. These features would make surrendering the contract in a single lump sum undesirable attributable to tax penalties.

A 1035 alternate to a extra favorable contract supplies an affordable resolution. You possibly can decrease your charges. Additionally, you will purchase time to proceed deferring taxation and to find out a extra tax environment friendly technique to get cash out of the annuity moderately than taking a lump sum multi function 12 months.

Selecting an Annuity?

A 1035 alternate generally is a good resolution to “make lemons out of lemonade” with an outdated annuity or life insurance coverage product you have been bought. However do these low-cost annuities should be thought of on their very own deserves? Usually, no.

There are two key causes for this: annuity charges and taxation of annuities.

Annuity Charges

Let’s take a more in-depth take a look at the charges on the annuity talked about. It is among the lowest price variable annuity merchandise available on the market, if not the bottom.

The commenter astutely factors this out, noting the distinction of .35% all-in for the variable annuity vs. .015% for a similar funding bought outdoors of the annuity. The commenter additionally accurately factors out that the distinction of .335% equates to a distinction of $335 per 12 months on a $100,000 funding.

Nonetheless, this overlooks (I imagine by accident) the identical factor that people who promote these contracts don’t clarify (I’m not as beneficiant in assuming it’s unintentional on their elements). That neglected part is the compounding of charges!

Let’s take into account the distinction between two in any other case similar $100,000 investments. Every compound at 8% per 12 months minus their respective charges for twenty years.

A $335 annual price for twenty years could be $6,700. However charges aren’t linear. They compound. Figuring out the precise affect of this price distinction requires a few time worth of cash calculations.

The cash invested within the variable annuity with all in charges of .35% would compound to $436,798. This identical amount of cash invested with all in charges of .015% would compound to $464,803.

The results of this seemingly small distinction in charges leads to ending with $28,005 much less after the twenty 12 months interval, all else being equal. If we compound the distinction out 30 years, the distinction grows to $89,186!

Anybody promoting annuities will likely be fast to level out that this isn’t a sound apples to apples comparability. Annuities are taxed otherwise than taxable investments.

That is true! Nonetheless, most often taxation is another excuse to keep away from annuities moderately than a motive to decide on them.

Taxation of Annuities

Funding features in an annuity are shielded from annual taxation. That is the largest tax benefit offered by an annuity.

In alternate for this profit, features on investments contained in the annuity lose favorable capital features tax therapy. Any features inside an annuity are in the end taxed as abnormal revenue when a withdrawal is taken, much like a non-deductible IRA. Additionally much like a retirement account, annuity withdrawals are topic to a ten% penalty on the features if taken earlier than age 59 ½.

As well as, annuity withdrawals are taxed on a last-in, first-out foundation. Because of this 100% of each greenback you’re taking from an annuity is taxed as abnormal revenue (and topic to early withdrawal penalties) till all the features are exhausted. At that time, the rest is a tax-free return of your principal.

In case you elect to annuitize funds, taxation is a extra difficult formulation the place every fee consists partially of taxable achieve and partially tax-free return of principal in your calculated life expectancy. In case you outlive your life expectancy, funds change into 100% taxable as abnormal revenue.

Annuities vs. Different Tax-Advantaged Accounts

Annuity features are taxed as abnormal revenue like a tax-deferred retirement account. Annuities include early withdrawal penalties much like certified retirement accounts. They don’t include the upfront tax deductions of conventional retirement accounts or tax-free withdrawals of Roth accounts.

Subsequently, there’s little motive to ever take into account shopping for an annuity in case you are not first maxing out all different tax-advantaged choices (work sponsored plans, IRAs, HSAs, and so forth.). They supply superior tax advantages, much less complexity, and customarily decrease charges.

There’s additionally no motive to ever purchase an annuity within a professional account for tax advantages. The tax advantages of the retirement account are already superior to these of an annuity.

In case you are an excellent saver who maxes out all of your tax-advantaged accounts, annuities can present some further tax advantaged house to protect your investments from the annual tax drag created by taxation of revenue produced inside a taxable account. Nonetheless, the worth of this tax profit comes with trade-offs that make this profit questionable at greatest.

Annuities vs. Taxable Accounts

How useful is utilizing an annuity to remove annual tax drag? The worth relies on a number of components.

The primary is what you intend to put money into. In case you are following the primary rule of thumb of using all of your accessible tax-advantaged accounts, they may present house to carry your least tax-efficient investments. You may use a taxable account to carry solely tax-efficient investments like an S&P 500 index fund as talked about within the remark.

On this case, most of your features will come within the type of capital features. Thus you will have tax-deferral on the most important portion of your funding achieve till you promote the funding. Extra importantly, you get this profit freed from cost and with out the complexity of annuity contracts!

Tax-efficient investments like broad based mostly index funds generate little to no annual capital features or non-qualified dividends. That by definition is why they’re tax-efficient. This leaves you with solely certified dividends that are taxed at favorable charges of 0%, 15%, or 20%.

The second issue when figuring out the tax good thing about an annuity vs. a taxable account is your private tax fee and the way it will change over time. In case you are saving aggressively in direction of early or semi-retirement, chances are you’ll very nicely pay 0% tax on taxable accounts in your decrease revenue years.

Associated: Understanding the Advantages and Drawbacks of Taxable Accounts

Earlier than contemplating an annuity for tax advantages, ensure you perceive the trade-offs this entails. You’ll be giving up favorable tax charges, presumably 0%, on long-term capital features and certified dividends in a taxable account to in the end pay abnormal revenue charges on any annuity features. You additionally need to weigh the unfavorable affect of annuity charges vs. any potential tax advantages the annuity supplies.

Ought to You Purchase an Annuity on Its Personal Deserves?

Few folks purchase advanced annuities like variable or fairness listed merchandise. Most frequently these contracts are bought by brokers who’re paid handsomely to take action.

These salespeople play on fears to spotlight options like “market-like progress” with restricted draw back and tax sheltered funding revenue. They downplay or outright omit discussing the affect of excessive annuity charges. They misrepresent the truth that in lots of instances there isn’t any precise tax profit. In truth, chances are you’ll pay extra tax by using an annuity!

Like this commenter chances are you’ll end up in possession of considered one of these contracts. You wouldn’t make an knowledgeable resolution to purchase this product immediately. In that case, using a 1035 alternate is a viable choice to start out recent in a extra favorable contract and permit for future tax planning.

Nonetheless, there’s hardly ever a motive to purchase even the bottom price variations of those merchandise on their very own deserves.

Associated: Annuities – The Good, The Unhealthy & The Ugly

* * *

Worthwhile Sources

- The Finest Retirement Calculators may help you carry out detailed retirement simulations together with modeling withdrawal methods, federal and state revenue taxes, healthcare bills, and extra. Can I Retire But? companions with two of the very best.

- Free Journey or Money Again with bank card rewards and enroll bonuses.

- Monitor Your Funding Portfolio

- Join a free Empower account to realize entry to trace your asset allocation, funding efficiency, particular person account balances, internet value, money movement, and funding bills.

- Our Books

* * *

[Chris Mamula used principles of traditional retirement planning, combined with creative lifestyle design, to retire from a career as a physical therapist at age 41. After poor experiences with the financial industry early in his professional life, he educated himself on investing and tax planning. After achieving financial independence, Chris began writing about wealth building, DIY investing, financial planning, early retirement, and lifestyle design at Can I Retire Yet? He is also the primary author of the book Choose FI: Your Blueprint to Financial Independence. Chris also does financial planning with individuals and couples at Abundo Wealth, a low-cost, advice-only financial planning firm with the mission of making quality financial advice available to populations for whom it was previously inaccessible. Chris has been featured on MarketWatch, Morningstar, U.S. News & World Report, and Business Insider. He has spoken at events including the Bogleheads and the American Institute of Certified Public Accountants annual conferences. Blog inquiries can be sent to chris@caniretireyet.com. Financial planning inquiries can be sent to chris@abundowealth.com]* * *

Disclosure: Can I Retire But? has partnered with CardRatings for our protection of bank card merchandise. Can I Retire But? and CardRatings might obtain a fee from card issuers. Different hyperlinks on this web site, just like the Amazon, NewRetirement, Pralana, and Private Capital hyperlinks are additionally affiliate hyperlinks. As an affiliate we earn from qualifying purchases. In case you click on on considered one of these hyperlinks and purchase from the affiliated firm, then we obtain some compensation. The revenue helps to maintain this weblog going. Affiliate hyperlinks don’t enhance your price, and we solely use them for services or products that we’re aware of and that we really feel might ship worth to you. In contrast, we’ve restricted management over a lot of the show adverts on this web site. Although we do try to dam objectionable content material. Purchaser beware.

[ad_2]