2024 Q1 Investor Psychology Commentary

by thebestworldevents.com 3 February 2024 · Wealth Management

[ad_1]

This text/video is a part of a collection that applies psychology to monetary planning so we will all make wealthier selections. As a multi-billion-dollar funding and planning agency, Mission Wealth can provide you collective knowledge and real-life examples from hundreds of multimillionaires.

Joey Khoury is certainly one of Mission Wealth’s Senior Wealth Advisors and a professor who has studied behavioral finance at Cornell and Harvard. Joey and Mission Wealth plan to publish 1-3 psychological matters which might be related to what’s occurring on the earth round us. To kick off the brand new 12 months, we selected the matters of holding money, market timing to keep away from in 2024, and whether or not worldwide battle ought to play into your funding selections.

Watch the Video Under

Matter #1: Money & Recency Bias

In 2023 the asset class that had essentially the most quantity of inflows was money, with a whopping $1.3 trillion of worth transferring to money positions final 12 months. Whereas a +5% curiosity on money appealed to many buyers in 2023, the anticipated rate of interest cuts over the following 12 to 24 months will show money to be a short-lived alternative. As rates of interest drop, this money should go someplace.

Buyers making an attempt to make this resolution by timing short-term business tendencies will seemingly be punished. Our brains are wired to make selections which might be over-reliant on the latest knowledge and occasions (a well-documented psychological error referred to as Recency Bias). This will get us into a complete lot of hassle after we begin making funding selections as a result of we regularly make long-term selections based mostly on short-term info.

Take, for instance, the big good points of development shares in 2023. The Vanguard Development Fund (ticker VUG) posted +46% in 2023. Buyers will seemingly examine this to the Vanguard Worth Fund (ticker VTV), which solely earned +9% in 2023. Buyers who discover this distinction might ask “Why do I maintain worth shares when development is doing so nicely?” If we rewind to 2022, a unfavourable 12 months, development was among the many worst performers (-33%) and worth was among the many finest (-2%). This led buyers to ask the precise reverse query: “Why do I maintain development shares when worth shares are a lot much less dangerous?”

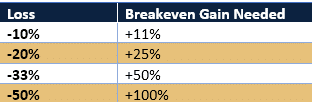

The 2-year returns over each 2022 and 2023 have been larger for worth shares than for development shares regardless of development shares posting +46% final 12 months. The important thing level: constructing a constant portfolio means much less of your {dollars} should work as exhausting to make up for prior losses. The extra you lose, the extra it’s a must to earn to interrupt even: a ten% loss wants an 11% acquire to interrupt even, a 20% loss wants a 25% acquire to interrupt even, a 33% loss wants a 50% acquire to interrupt even, and a 50% loss wants a 100% acquire to interrupt even.

Whereas it may be uncomfortable to systematically promote whereas the worth is excessive and purchase whereas the worth is low and (a course of referred to as rebalancing), historical past exhibits that it could possibly create a smoother experience and comparable cumulative returns to the market. Over a number of years, avoiding the massive market busts might be extra worthwhile and emotionally simpler than chasing the massive booms.

Take this comparative pattern portfolio with 60% within the inventory markets and 40% within the bond market versus the S&P 500 since 2000. In optimistic markets, buyers really feel dangerous about not incomes as a lot because the S&P 500. In unfavourable markets, buyers aren’t completely happy about shedding any cash in any respect (even when their diversified portfolio didn’t go as far down as the final market). There’ll at all times be a cause to be sad with relative efficiency when instances are each good and dangerous.

The important thing takeaway: when making funding selections, it’s finest to take a longer-than-one-year perspective. In the event you can preserve a 3–5-year give attention to funding selections, you’ll be doing your self a monetary favor with much less of an emotional experience.

Matter #2: Gambler’s Fallacy & Recency Bias

Final 12 months (2023) the S&P 500 grew by about 24% and ended on a really optimistic notice within the fourth quarter. Issues that 2024 can be a unfavourable 12 months to compensate have began to bubble up. Whereas no one has a crystal ball to foresee the market efficiency on a short-term foundation, some historical past of how markets have behaved can assist information how we take into consideration this ‘reversion threat’.

Merely put, the markets don’t comply with a calendar like we do. For my fellow nerds, knowledge doesn’t point out that imply reversion happens on an alternating calendar 12 months foundation.

Listed here are some key factors from the historical past of optimistic and unfavourable years within the S&P 500 since 1928:

- Markets have been optimistic about 73% of the time and unfavourable about 27% of the time. Enjoying the lengthy recreation means staying the course whenever you’re within the pink 27% of the time, realizing that the bigger variety of good instances outweigh the dangerous instances.

- Markets are solely back-to-back unfavourable about 9% of the time.

- When markets have a optimistic 12 months, they’ve traditionally adopted with one other optimistic 12 months 54% of the time and adopted with a unfavourable 12 months solely 19% of the time.

With historical past as a information, this can assist you contextualize the urge to assume that we’re ‘overdue’ just because the prior 12 months was optimistic. However nonetheless, there are headlines of crises all world wide. Certainly these will contribute to unfavourable markets, proper? This brings us to our third and closing subject for this quarter: worldwide battle.

Matter #3: Worldwide Battle & Salience Bias

Billy Joel mentioned it finest: “We didn’t begin the fireplace; it was at all times burning because the world’s been turning”. Wars, famine, pure disasters, political rebel, and protests attain international consideration with know-how permitting us to immediately talk from any nook of the world. The problem is that all of us face Salience Bias, which is our inclination to present an excessive amount of significance to emotionally impactful info.

Whereas sympathizing with humanitarian crises, many buyers additionally develop involved with how worldwide battle might have an effect on their life financial savings. Russia and Ukraine, Israel and Palestine, protests in Iran, pure disasters in Japan, rebellions within the Democratic Republic of Congo, and so many extra headlines that may make you need to bury your head within the sand.

In the end, chances are you’ll marvel: How a lot does worldwide battle have an effect on the U.S. inventory market? To reply this, we tracked how a lot income every nation contributed to the income of the S&P 500.

Greater than half of the income from U.S. Giant Firms was generated inside the US. In complete, there are solely 9 international locations that exceed a 1% contribution to the S&P 500 income. These are China at 8%, Japan at 2.9%, the UK at 2.4%, Germany at 2.3%, Canada at 1.8%, Taiwan at 1.7%, India at 1.5%, France at 1.4%, and South Korea at 1.1%. Outdoors of the highest 9 international locations, the opposite 185 international locations contribute a complete of 20% income. That’s a median of 0.11% per nation listed within the ‘different’ class.

What does this imply? Take the battle in Russia and Ukraine or Israel and Palestine. These international locations match into the ‘different’ class, with a median S&P 500 income of 0.11% per nation. The market income isn’t impacted by these international locations as a result of the businesses inside the market don’t supply a lot income from these international locations. This doesn’t imply that we will’t care from a humanitarian perspective. As a substitute, it signifies that the U.S. market is usually unbiased, and that the worldwide income produced by U.S. Firms is well-diversified throughout the globe.

In instances of turmoil, U.S. markets have traditionally shrugged off worldwide battle. Courting again to 1939, knowledge analyzing what occurs to the S&P 500 round dozens of geopolitical occasions point out that on common the U.S. market tends to take simply 3 weeks to achieve a backside and one other 3 weeks to recuperate to prior ranges.

To call a number of examples: it took the S&P 500 9 days to recuperate from 2016’s Brexit, 16 days to recuperate from the 2003 warfare in Iraq, 9 days to recuperate from the 1962 Cuban Missile Disaster, 1 day to recuperate from JFK’s assassination in 1963, 14 days to recuperate from the 2014 Ukraine battle, and 15 days to recuperate from the 911 assaults in 2001. Within the 12 months following geopolitical occasions, the market earned +13% on common.

Even with this crystal-clear knowledge, some buyers should be involved about U.S. authorities spending on worldwide battle. Right here’s how materials our international support is relative to our federal funds and GDP:

- In 2023 the federal authorities funds for worldwide support was about $60B, which was about 1% of the $6.1 trillion complete federal funds.

- All of presidency spending accounts for about 25% of the U.S. GDP.

- Since international support is simply about 1% of complete authorities spending, and complete authorities spending makes up lower than 25% of our GDP, the entire influence of international support spending on our GDP is lower than 0.25% (1% x 25%).

There stays 99.75% of our GDP unaffected by international support. But, there are not any articles on-line that may contextualize this. We will get caught within the crosshairs of the attention-seeking media headlines when most international locations characterize lower than 1% of our market’s income, international support represents lower than 1% of the federal funds, and worldwide spending on support represents lower than 0.25% of our GDP.

We hope you discovered these matters useful as we enter the brand new 12 months. For extra detailed market commentary, we welcome you to learn or watch our Chief Funding Officer’s market updates from our Insights Weblog.

To submit a request for future matters, please don’t hesitate to e mail Joey instantly at jkhoury@missionwealth.com.

[ad_2]